Become a

Smarter

Investor

in 15 Minutes

Free guide helps you unlock the potential

of your retirement account

– all before you

finish a cup of coffee.

X

Call an IRA Counselor

Hours: Monday-Friday,

8am-6pm (ET)

Schedule a Discovery Call

Access 15-Minute Guide to

Self-Directed IRAs

By entering your information and clicking Download Guide, you consent to receive reoccurring automated marketing text messages and emails about Equity Trust’s products and services. This consent is not required to obtain products and services. If you do not consent to receive text messages and emails from Equity Trust and seek information, contact us at 855-233-4382. Reply STOP to opt out from text messages. Message and data rates may apply. View Terms & Privacy.

Real estate investments can come in many forms, making it easy to find one that fits your interests. Talk to an IRA Counselor about the broad range of real estate assets that can be held in an IRA or other retirement account. Self-directed IRA real estate investments can include:

Real estate can be a profitable, rewarding way to grow your self-directed account and potentially help you achieve your dreams faster.

Real estate has historically generated higher returns than traditional/public market investments

Hedge against public investments with an investment not tied to stock market performance

Turn your expertise or a passion for real estate into revenue for your retirement account

Our clients’ accounts fund neighborhood revitalization and provide affordable housing

Many projects create jobs for local contractors and other service providers

From managing rehabs to lending money to real estate investors, there’s a variety of investment options

Equity Trust enables you to easily invest in real estate using your self-directed IRA or other account, tax-deferred or tax-free.

Here’s what you need to know to reap the benefits of this powerful investment type in your self-directed account:

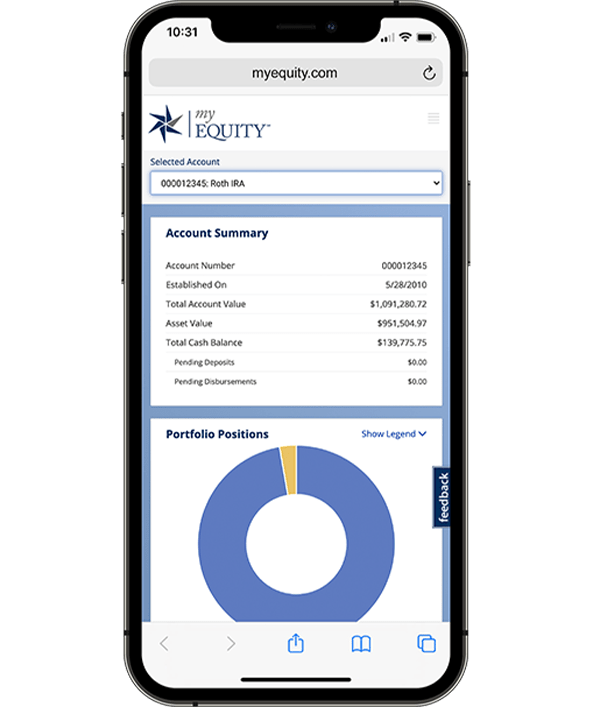

One of our specialized counselors will walk you through the process, or you can do it online with myEQUITY.

A few potential sources:

Possibilities include:

Easily initiate your investment with the Real Estate Wizard in myEQUITY.

Our liaisons are here to help you if you need it.

Equity Trust Client

“I never knew that investing my retirement into real estate could be this easy. Equity Trust Company made the process so seamless and pleasant that I can’t stop talking about it to friends and family…”

Equity Trust Client

“This is a bit of a new experience for me so their [associates] were extremely helpful in answering all of my questions promptly and accurately. The bill pay service is very user friendly and extremely easy to use.”

Equity Trust Client

“My real estate transactions were top-notch and all bills were paid in a very timely manner, extremely effortless, with no issues. My only regret is that I didn’t know about self-directed IRAs years ago, but I’m happy I finally found out about Equity Trust!”

Equity Trust Client

“Our real estate purchase is now complete… I’ve paid a couple of transaction related bills through Equity Trust and I am surprised at how easy it has been and how completely Equity is managing the accounting, bill payment, and even the task of mailing items. I am not a financial guy, but I feel like this has been a very solid decision.”

Equity Trust Client

“We have held IRAs with Equity Trust Company for over 20 years. They are the LEADER in the industry with service, knowledge and education!”

Equity Trust Client

“Investing in a self-directed IRA is the best kept secret! The process to purchase real estate using my IRA savings is fairly simple and after flipping the property, all profits remain in the IRA account without capital gains. It’s a win-win for me since I left my corporate job and don’t regularly make contributions. This works!”

Buying real estate with an IRA has never been faster, easier, or more streamlined. Our state-of-the-art online account management system enables you to:

What are you investing for? Whether your “why” is retirement, healthcare expenses, or a loved one’s education, we make the journey easy with innovative technology and first-class service.

Traditional financial institutions limit your account to traditional investments. With Equity Trust, you can truly diversify into a range of options including real estate, private entities, cryptocurrency, precious metals, and more, in addition to stocks, bonds, and mutual funds – all in one account.

Our size, expertise, and technology help us ensure that we’re there when you need us most. With more than 400 associates focused on processing over 2 million transactions each year, we work diligently to enhance your experience with us.

Our knowledgeable, client-focused associates are here to provide dedicated, personalized service, from opening your account to assisting you with investment transactions. You can lean on our 50 years of experience in the financial services industry. Talk to a knowledgeable IRA Counselor.

Don’t have an investment in mind? Most custodians establish your account and leave you on your own to figure it out. Our WealthBridge portal and Investment District online marketplace enable you to find potential investment opportunities with the click of a button. Start your search

We don’t stop at providing a superior investing experience: Each client receives access to exclusive opportunities not found with any other self-directed account custodian. You’ll receive valuable, in-demand discounts and membership access – just for opening an account.

Let our industry-leading education and resources help you navigate through your real estate investing journey.

Learn how it works, read a real-life example, and how to get started.

Browse the tax-advantaged accounts and find one that matches your savings goals – from retirement to education to health care savings.

Dig deeper into how real estate investing works in a self-directed account.

Ready to Get Started?

Our knowledgeable IRA Counselors can answer your questions about the self-directed investing process and share insight and education about our self-directed accounts to help you decide what options may be best for you.

By entering your information and clicking Start a Conversation, you consent to receive reoccurring automated marketing text messages and emails about Equity Trust’s products and services. This consent is not required to obtain products and services. If you do not consent to receive text messages and emails from Equity Trust and seek information, contact us at 855-233-4382. Reply STOP to opt out from text messages. Message and data rates may apply. View Terms & Privacy.

1 Equity WayWestlake, OH 44145

Terms of UsePrivacy PolicySite Map

© 2024 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 1/1/2024. 1ici.org, total assets in IRAs as of 12/2023

Terms of UsePrivacy PolicySite Map

© 2024 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 1/1/2024. 1ici.org, total assets in IRAs as of 12/2023

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.

Continue

Browse platforms and providers in private equity, cryptocurrency, lending, real estate, and precious metals asset classes – all in one place.