Become a

Smarter

Investor

in 15 Minutes

Free guide helps you unlock the potential

of your retirement account

– all before you

finish a cup of coffee.

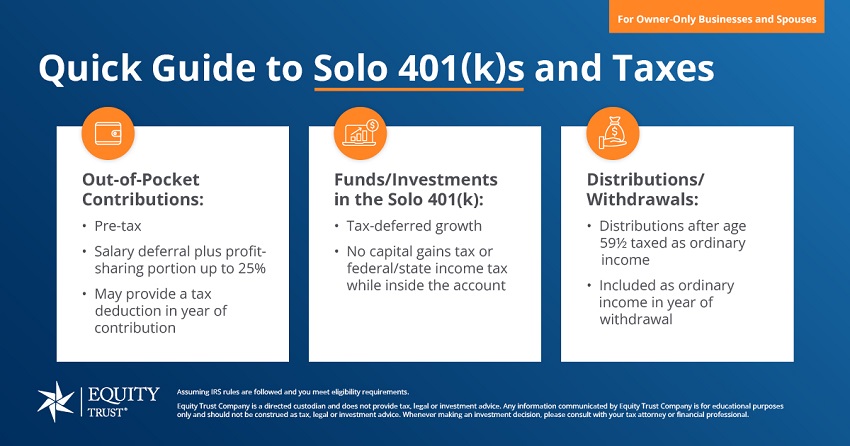

The self-directed Solo 401(k) (also known as Individual 401(k), Self-Employed 401(k), and Solo(k)) is often the most attractive plan to investors, if they qualify, because it combines elements of the SEP and SIMPLE.

The Individual 401(k) is designed for owner-only businesses and spouses. It can be established by both incorporated and unincorporated businesses, sole proprietorships, partnerships, and corporations.

If you qualify, the Individual 401(k) plan offers higher contribution amounts and possible tax deductions.

Two components comprise the maximum Individual 401(k) plan contribution:

The total annual contribution limit from both sources, for those under age 50, is $69,000 in 2024.

The Individual 401(k) is for incorporated and unincorporated businesses, sole proprietorships, partnerships, and corporations. The only requirement for contributions to this plan is that you receive a salary or wage.

The business entity must have no additional employees other than the spouse of the proprietor—or, in the case of a partnership, the only employees must be self-employed partners and their spouses.

An Individual 401(k) plan must be the only arrangement maintained by the business that is not included as part of a controlled group under federal tax law.

The deadline for establishing an Individual 401(k) plan is the last day of your business’s tax year (December 31, for a calendar tax year).

However, if your business is incorporated, you may want to establish an Individual 401(k) plan early in the tax year to make employee salary deferrals based on the Form W-2 income throughout the year.

This is necessary because you may not defer on compensation that is paid to you from your corporation before you establish the Individual 401(k) plan.

When a Solo 401(k) is referred to as a self-directed account, it simply means you can use the account invest in areas outside of the traditional stocks and bonds. That’s the primary difference between a self-directed and traditional retirement account — where you put those investment dollars.

With a self-directed Solo 401(k) or IRA, you can invest in a variety of areas, including:

If you’re interested in opening a self-directed Solo 401(k), or for more information about this plan, please contact a Specialist at 855-233-4382.

In this session, you’ll learn about:

Let’s talk about your financial future.

Schedule a one-on-one session with an expert alternative investment counselor. We’re here to answer any questions, help guide you through the process, and provide more detailed information and education specific to your journey.

By entering your information and clicking Start a Conversation, you consent to receive reoccurring automated marketing text messages and emails about Equity Trust’s products and services. This consent is not required to obtain products and services. If you do not consent to receive text messages and emails from Equity Trust and seek information, contact us at 855-233-4382. Reply STOP to opt out from text messages. Message and data rates may apply. View Terms & Privacy.

1 Equity WayWestlake, OH 44145

Terms of UsePrivacy PolicySite Map

© 2024 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 1/1/2024. 1ici.org, total assets in IRAs as of 12/2023

Terms of UsePrivacy PolicySite Map

© 2024 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 1/1/2024. 1ici.org, total assets in IRAs as of 12/2023

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.

Continue

Browse platforms and providers in private equity, cryptocurrency, lending, real estate, and precious metals asset classes – all in one place.